Every Friday I posting the latest enrollment figures for the Affordable Care Act (aka Obamacare) here at Eclectablog. Full details can be viewed daily at ACASignups.net.

This has been the craziest week yet for ACASignups.net, and the past day or so, things went into overdrive.

If November had an Obamacare surge, consider this the December deluge. California averaged 15,000 daily enrollments early last week, about double the sign-ups the state had in early December. New York is now seeing about 4,500 residents choosing plans each day and, in Connecticut, the number is hovering around 1,400.

That bumped the number of private plan enrollments up to 815,000.

Then came Washington State, which is now up to either 32K or 93K, depending on your definition (WA is the only state to *specifically* define “enrolled” as having already made your first payment; every other state logically recognizes that if you buy a new car with a “$0 down” deal, it’s still considered a sale as far as the dealer is concerned). WA along with new figures from Minnesota and Maryland moved the dial up to 860,000.

The Minnesota numbers are extremely telling for another reason. Check out this passage from the linked article:

By Dec. 14, 11,805 people had signed up for private plans — more than twice the 4,478 private policies that had been purchased by the end of November. That’s in addition to 27,150 people who signed up for the state’s two public insurance plans through MNsure.

The agency estimates that in all, those sign-ups translate to 97,573 people who will be covered since many plans cover more than one family member.

This is one of the only articles that’s specifically listed both the number of *enrollments* as well as the number of *people covered by those enrollments*, and it’s showing nearly a 3x difference. How many of the other numbers reported for other states should be 2-3x higher? I have no way of knowing; we won’t find that out until the next official HHS report.

According to government figures, about 680,000 people had enrolled in plans through the federal insurance exchange as of earlier this week. That means that nearly 550,000 people signed up this month; figures released by the HHS show that about 137,000 people had chosen a health plan by the end of November.

Holy Moly. Unfortunately, this figure leaves out one crucial detail–how many of those 550,000 (actually closer to 543,000) enrollees are for private plans as opposed to Medicaid/SCHIP expansion? If it includes both, then it’s likely a 30/70 split with around 370,000 belonging on the Medicaid side. The context of the paragraph it’s in suggests that these are all private plans, but that’s too large a number to categorize without being sure.

As a result, until I receive confirmation one way or the other (I’ve emailed the journalist asking for clarification but haven’t heard back yet), there’s a lengthy note next to the figure on the spreadsheet and a special colored area on the graph below.

And finally, late last night came the capper out of California:

SACRAMENTO, Calif. — With the deadline approaching for Covered California™ health insurance coverage beginning Jan. 1, 2014, tens of thousands of new enrollees are seeking out help and signing up for plans. In fact, preliminary data indicates that in just the past three days (Dec 16-18), 53,510 people enrolled by selecting a Covered California health insurance plan. That tops the 30,830 enrollments completed for the entire month of October by nearly 60 percent.

The 15K per day average from last week was extremely impressive. This just upped the ante even more, culminating in the key line:

On Wednesday, Dec. 18, a total of 20,506 enrollments were received by Covered California

Over 20K.

In one day.

From one state.

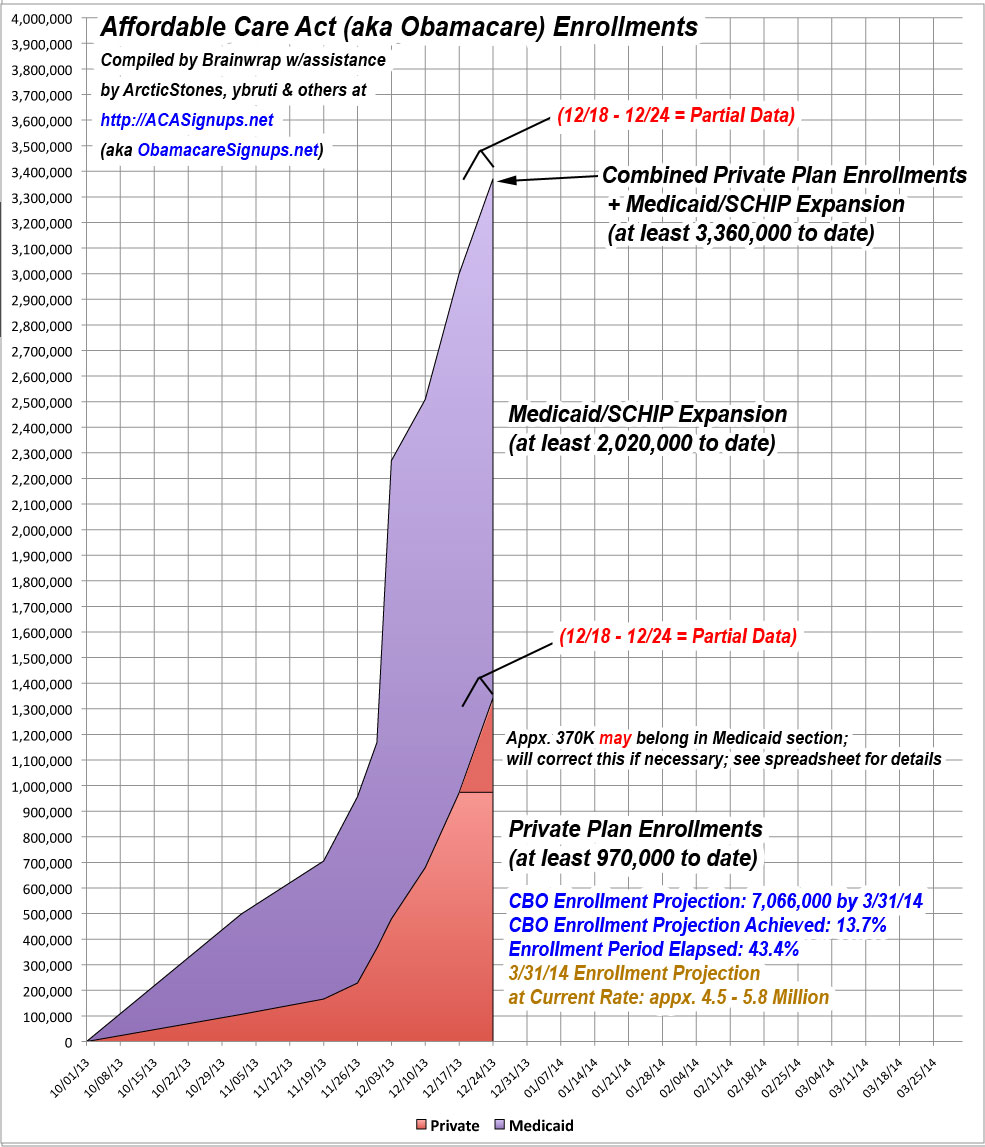

Anyway, here’s where things stand as of 10:00am Friday morning. Given the news of the past few days, even this could be obsolete by, oh, 10:05am:

Private Enrollments: 970K (or 1.34 million)

Medicaid/SCHIP Expansion: 2.4 Million (or 2.0 million)

Total either way: 3.36 Million