You’re traveling through another dimension, a dimension not only of sight and sound but of mind. A journey into a wondrous land whose boundaries are that of imagination. That’s the signpost up ahead— your next stop, the Hypocrisy Zone!

Things have really gotten hypocritically bizarre in Republican attempts to undermine the Affordable Care Act. Pundits across the country are outwardly laughing at the GOP’s about face. Where they once demonized, impeded, and attempted to destroy the new health insurance law, they are now displaying faux poutrage that it isn’t rolling out perfectly, even to the point of holding Congressional hearings on it. Americans United for Change expresses it perfectly in an email today titled “Spare Us the Crocodile Tears, Congressmen Upton, Rogers”:

Hypocrisy red alert. Just days after Republicans in Congress shut down the government in the latest in a long string of attempts to kill or cripple the Affordable Care Act, Republicans on the House Energy and Commerce Committee, including Mike Rogers (R-MI-8) and the committee’s Chairman Fred Upton (R-MI-6), are holding a public hearing this morning billed as the “the failures and issues surrounding the implementation” of the health law.Many Americans are left wondering today, what’s more absurd? : 1) the fact that Republicans in Congress are already declaring efforts to enroll Americans in the health law’s insurance exchanges a ‘failure’ just 24 days into the six month process, or 2) the fact that Republicans are actually complaining about implementation glitches when they opposed the Affordable Care Act at its inception, have done everything in their power to delay, repeal, defund the law every day since, have repeatedly blocked funding needed for implementation, and whose entire health plan is to let the insurance companies go back to denying coverage to millions of Americans with pre-existing conditions and dropping people when they get sick…It’s really rich for Congressmen Upton and Rogers to be shedding crocodile tears over the glitches in the ACA website when they have done nothing for four years but try to impede, repeal and defund the law and root for its failure. This is pure, craven politics.

Indeed.

Congressman John Dingell, the Dean of the House, made this amazing statement at today’s hearing:

For the last few years my Republican friends have called the Affordable Care Act a ‘job killer,’ a ‘threat to liberty,’ and that it would ‘pull the plug on Grandma.’ They have said things like ‘We have to do everything in our power to prevent Obamacare,’ and ‘Obamacare. Get rid of it. Period.’All of the sudden, our friends on the other side of the aisle have forgotten this, and are now focused on the successful implementation of the law and the problems it faces. This is encouraging, and I hope this is a sign that we can work together on this critical issue.

Let me be clear: I am as frustrated as anybody with the problems facing Healthcare.gov. This is unacceptable and needs to be fixed, and we can do it. But a slow website is still better than the alternative, where healthcare is a privilege for a select few, rather than a fundamental right for all.

I look forward to exploring how the website can be fixed during this hearing today, and hope my Republican colleagues will be constructive participants in this process, rather than continuing their destructive opposition to the law.

One group calling themselves the American Center for Law and Justice (“specifically dedicated to the ideal that religious freedom and freedom of speech are inalienable, God-given rights”) even has a website up where you can report problems with the new health insurance exchanges called ICantEnroll.com.

The anti-Obamacare trolls are rolling out across the internet, even on this site, telling stories of draconian health insurance rate increases without proof as if the plural of “anecdote” is “data”. If that were the case, we have plenty of “data” of our own in stories told of incredible savings being had by countless people on progressive sites like Daily Kos and elsewhere. Rene Greff, who owns the Arbor Brewing Company and the Corner Brewery in Washtenaw County, Michigan, for example, posted this to her Facebook page:

So after a decade of meeting with our insurance broker every year for our annual renewals and having to choose between 25% premium increases or further erosion of benefits I am so excited that this year’s meeting was entirely different.Having heard all of the horror stories about the Affordable Care Act, I was expecting the worst but according to our broker, when next year’s renewal rolls around we will actually have real choices that are going to save the business and our employees money, give us all a lot more choice in terms of the individual plan options that we want, and best of all, now more than 15% of our staff will have access to insurance.

I can’t believe the government finally did something to benefit small business!

Or this from former Fox Contributor Sally Kohn:

Three years ago when I was shopping for insurance, there weren’t that many options to choose from. And the plan I ended up with is expensive and, to put it bluntly, crappy.Currently, I pay $965 per month for family coverage that includes:

- a whopping $7,000 deductible;

- $36,000 out-of-pocket max per year;

- an annual coverage limit of $2,000,000;

- a $35 co-pay for doctor’s visits ($55 for specialists); and

- a $15 co-pay for generic prescriptions.

[…]

For a few days, I couldn’t do anything at all on the website.

Then for a day or so I could “log-in” but not complete registration. And then for a day, I could answer the questions to complete my registration but not actually complete the process.

On one occasion, I got so frustrated at the stalled exchange website that I actually shook my computer.

Not pleasant.

But finally, early on the first Saturday morning following the launch of the exchange site — probably because the rest of the state (unlike my five-year-old) was still asleep — I was able to log-in and complete my registration and check out all my options for insurance.

There were literally 50 plans that were better than my current insurance — both with lower premiums, lower out-of-pocket costs and better coverage. And there were ten plans with a higher premium than my current insurance, but with lower deductibles.

So — and here’s an important point — the reason that more people haven’t signed up for coverage yet is probably that, just like me, they needed to take some time (and first, find some time!) to weigh all the options.

While the exchange site was user-friendly and explained my options in a clear and simple way, picking an insurance plan isn’t exactly like ordering a hamburger. It took a minute to find my calculator and think about the options.

Within a week, I had settled on a “gold” plan offered by Empire Blue Cross Blue Shield. The plan includes:

- a $2,000 total deductible;

- an out-of-pocket max of $12,500 for the year;

- a $30 co-pay for visits to our primary care doctor;

- a $15 co-pay for generic prescriptions;

- NO annual coverage limit — because that’s now prohibited thanks to the Affordable Care Act; plus

- an added bonus: the plan I selected includes child dental.

This option will cost my family $931 per month — $408 per year less than my previous crappy plan and a $5,000 savings in deductibles. A big win for me and my family financially and in terms of what’s covered.

People that are experiencing increases in their premiums likely, as Consumer Reports explains, have bad information:

I’ve heard from many readers who say their health insurance premiums are going through the roof because of the new health law, and they’re having their doubts about the “affordable” part of the Affordable Care Act.But when they’ve given me enough information to look into their situation, in almost every case it turns out they’re upset over nothing—because their health costs are not going up after all. They just haven’t been able to find their way to the right information. […]

[I]n the meantime, use our interactive tool, Healthlawhelper.org. It will tell you right away what kind of help you may have coming to you, and possibly ease your mind.

Anti-Obamacare trolls tried to spin the piece as if it were proof of its failure. Consumer Reports was having none of it:

Obamacare opponents have misrepresented Consumer Reports' position #ACA @healthlawhelper http://t.co/Q7Hr3EN7QH

— Consumer Reports (@ConsumerReports) October 21, 2013

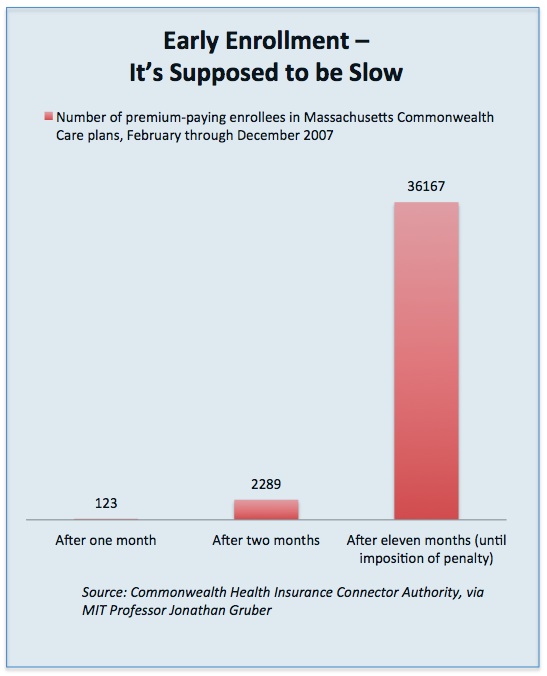

All of the faux hysteria over the flubbed rollout of the exchanges ignores the fact that we’ve seen this before. When Massachusetts rolled out its version (“Romneycare”) that now has the vast majority of its state enjoying affordable health insurance, it took nearly a year for it to take off. Check out this chart from a Jonathon Cohn piece in the New Republic:

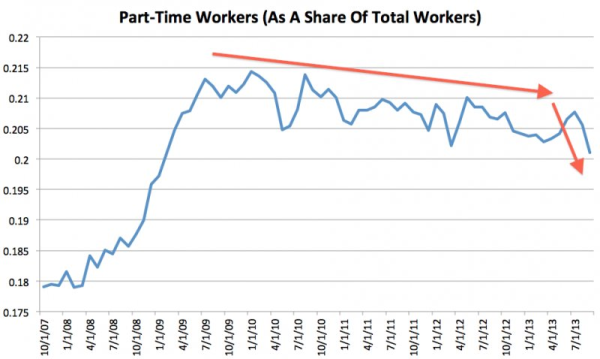

There’s also much ballyhoo about how Obamacare is going to lead to a “part-time economy” as millions of Americans are reduced to part-time work so their employers can avoid paying for their health insurance. As it turns out the opposite is true. The trend toward companies pushing their employers to part-time began well before the ACA was passed and, in fact, the trend is REVERSING:

[Graph by Business Insider using data from the Bureau of Labor Statistics]

The freakout over our new “part-time economy” ignores the fact that the employer mandate doesn’t even start for nearly a year and only affects companies with 15 or more employers. If they want to attract quality employees, you can be sure they’ll offer them more than part time employment.

Republicans add to the hypocrisy by failing to admit their own role in the issues healthcare.gov is experiencing:

“It is a mess and there’s no sugarcoating it, and people shouldn’t sugarcoat that,” says Jay Angoff, who formerly ran the health exchange program for the Department of Health and Human Services. “On the other hand, people should remember that those who are in charge of the money HHS needs to implement the federal exchange are dedicated to the destruction of the federal exchange, and the destruction of the Affordable Care Act.”Which led to the first big problem — money. When it became clear that HHS would need more money to build the federal exchange than had been allocated in the original law, Republicans in Congress refused to provide it.

As a result, says Angoff, officials “had to scrape together money from various offices within HHS to build the federal exchange.”

Then there was the timing issue. Technically, department officials have had 3 1/2 years since the law passed. But much of that time was spent in limbo. First there was waiting to see if the Supreme Court would overturn the law in the summer of 2012. (It didn’t.) Then there was waiting to see if Mitt Romney and a Republican Senate would be elected that November to repeal it. (They weren’t.)

Then it was another month waiting for states to decide if they wanted to build their own health exchanges or let the federal government do it for them.

There’s much more to this story which Ezra Klein masterfully explains in “The GOP’s Obamacare chutzpah” this morning at the WonkBlog:

The classic definition of chutzpah is the child who kills his parents and then asks for leniency because he’s an orphan. But in recent weeks, we’ve begun to see the Washington definition: A party that does everything possible to sabotage a law and then professes fury when the law’s launch is rocky.

Read the whole piece. It’s tremendous.

(By the way, if you’re interested in the ins and outs of problems healthcare.gov is experiencing, the Washington Post’s Sarah Kliff has laid it all out in a great piece, “Everything you need to know about Obamacare’s problems”.)

It’s truly an amazing spectacle to behold, watching the Republicans turning on a dime and exhibiting a sudden depth of care for the uninsured and under-insured in America that just a month ago was nowhere to be found. But, in the Hypocrisy Zone, apparently, what you’ve done and said in the past doesn’t exist. It truly is a “journey into a wondrous land whose boundaries are that of imagination” and Republicans have nothing if not incredibly vivid imaginations.

I can’t wait until they start complaining about healthcare.gov’s fonts.